Contents

Key Takeaways:

- Mine-site principal contracts routinely demand $20 million public liability, and that high limit for a sole-trader subcontractor sits outside most of the standard market.

- Tank recently placed $20M public liability for a WA poly-welding contractor after eight insurers in the mainstream market declined to quote.

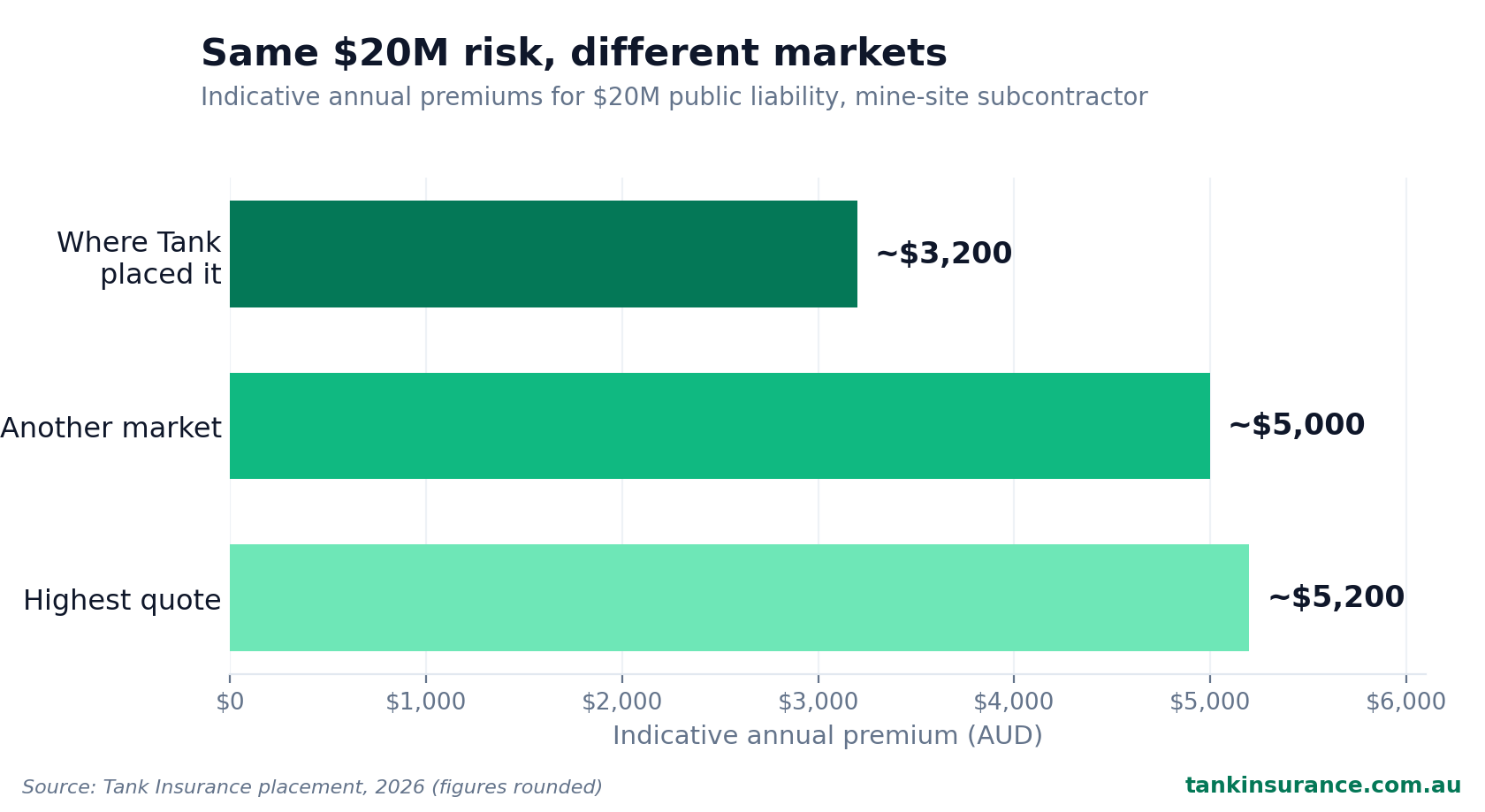

- Comparable quotes for the same cover ran from about $3,200 to over $5,000 a year. We placed it at the bottom of that range, around $3,200.

- Indicative terms came back within about a day. The bind hinged on one thing: the client’s ABN had to be registered and active before the underwriter would issue the policy.

Can a sole trader working on mine sites actually get $20 million public liability insurance? Yes, but it’s genuinely hard to place, and the standard market will often decline before it quotes.

We know because we just did it. A Western Australian poly-welding contractor came to us needing $20 million public liability for mine-site work, eight insurers in the mainstream market had no appetite for it, and we placed the cover with a specialist underwriting agency, with indicative terms back within about a day.

Here’s the full story: why mining contractors need such a high limit, why it’s so hard to place, what we did, and the last-minute ABN snag that nearly delayed the bind.

Why do mining contractors need $20 million public liability?

Most mine-site principal contracts require subcontractors to hold $20 million public liability before they’re allowed on site. It’s a contractual gate, not a legal minimum, but in practice you can’t start work without it.

Public liability covers third-party injury and third-party property damage caused by your work. On a mine site, the stakes are high: heavy plant moving around, expensive infrastructure, and a lot of other people on the ground. If a contractor’s work caused an injury or damaged a piece of mine infrastructure, the dollar figures get big fast.

That’s why principal contractors set the bar at $20 million rather than the $5 or $10 million you might see on a suburban building site. They’re protecting themselves and the site, and they push that requirement down the contractor chain. If you’re a subcontractor, the mine operator’s contract becomes your insurance brief.

For most trades, $20 million public liability is a step up from what they’ve held before. Many sole traders are used to $5 or $10 million, so the first time a mine engagement lands, the limit alone can be a shock.

Why is public liability for mining contractors hard to place?

Public liability for mining contractors is hard to place because three things stack up at once: a high-risk environment, a high required limit, and often a sole-trader structure. Put together, that combination sits outside the appetite of most standard insurers, so they decline rather than quote.

Standard public liability insurers are comfortable with $5 to $10 million for everyday trades. Ask them for $20 million on a mine site for a one-person business and many simply don’t have the appetite for it. It’s not that the risk is uninsurable. It’s that it doesn’t fit the boxes their automated and lower-touch facilities are built for.

In the placement below, eight insurers in the mainstream market declined to quote. That’s not unusual for this kind of risk. Once the standard market steps back, the cover has to be marketed to specialist liability underwriting agencies that are set up to underwrite higher-limit, higher-hazard work by hand.

A specialist liability underwriting agency is an underwriter that writes business on behalf of an insurer, usually for risks that need manual assessment rather than an off-the-shelf quote. These are the markets that can actually look at a mine-site contractor and price the cover properly, but you generally need a broker to access them.

The reality: high-limit public liability for a sole-trader mine-site subcontractor is one of the harder placements in the liability market. Getting a decline from the standard market isn’t a dead end. It usually just means the risk needs a specialist. We see it often, like a $20 million public liability placement for an earthmoving contractor that also had to go to a specialist market.

How we placed $20M public liability for a WA mine-site subcontractor

In late April 2026, a sole-trader poly-welding contractor in Western Australia called us. The job: $20 million public liability so they could keep working on mine sites. We had indicative terms back within about a day.

Here’s who they are. A plastic-fusion specialist with around 20 years’ experience, welding and supporting HDPE poly pipe on iron ore, gold and lithium mine sites across WA. They work 100% off-site as a subcontractor, with annual revenue around $200,000. No workshop. No hot-works permits. No earthmoving. The job is welding poly pipe and lifting and supporting it into position.

That detail matters more than it sounds. When the standard market hears “mine site,” it often assumes the worst and walks away. So the first thing we did was get the occupation described accurately to underwriters: off-site only, poly-pipe welding, no fabrication workshop, no hot works, no plant. We worked through the detailed questions each underwriter asked. Which mine types. What machinery, if any. Whether there was any earthmoving (there wasn’t).

We marketed the risk to around a dozen markets, including specialist liability underwriting agencies. Comparable terms came back ranging from around $3,200 to over $5,000 a year for the $20 million limit. We placed the cover with a specialist liability underwriting agency at the bottom of that range, approximately $3,200, with the option to pay around $260 a month instead of annually. The most expensive market we saw was over $5,000, so getting the description right made a real difference to the price.

Public liability is one of the products Tank places most often, but a $20 million limit for a sole-trader mine-site subbie is at the genuinely hard end of that spread.

The result: $20 million public liability, placed at approximately $3,200, with cover effective 2 May 2026 once the client’s ABN was active.

What can hold up a mine-site public liability placement?

On this one, it wasn’t price or appetite. It was the ABN. We had terms quickly, but they were subject to the client having an active ABN, and the client was still in the process of getting theirs sorted.

That’s a common condition. Many underwriters will give indicative terms without an active Australian Business Number, but they make it a subjectivity that the ABN is registered and active before they’ll bind the final policy. It’s how they confirm you’re a trading entity, so a lapsed or cancelled ABN has to be sorted before cover can start.

So we locked in the terms, kept the client updated while they got their ABN active, and bound the cover the moment it was confirmed. Cover was effective 2 May 2026.

If you’re a contractor heading into a mine engagement, it’s worth sorting your ABN early. You can check your status on ABN Lookup, and a cancelled or inactive ABN can be reactivated through the Australian Business Register (ABR). You don’t want it to be the thing standing between you and a start date.

Three things that smooth a hard-to-place mine-site placement

- Accurate occupation description - off-site vs workshop, hot works vs none, plant vs none. Underwriters price what you tell them, so vague descriptions get conservative pricing or declines.

- An active ABN - confirm it’s registered and active before you’re ready to bind, not after.

- Time - mine-site contracts have start dates, and specialist placements take a bit of marketing. Starting early beats scrambling.

What does $20M public liability cost for a mining contractor?

For a sole-trader mine-site subcontractor in 2026, comparable quotes for $20 million public liability ranged from around $3,200 to over $5,000 a year. We placed the cover at the bottom of that range, approximately $3,200, with a monthly option of around $260 a month.

Your number will sit somewhere in its own range, because public liability for mining work isn’t priced off a single rate. The main drivers are your trade and how hazardous it’s treated, your annual revenue, the mine types you work on, the machinery you operate, and whether any earthmoving or hot works is involved.

| Factor | Pushes premium up | Keeps premium down |

|---|---|---|

| Occupation | Fabrication, hot works, plant operation | Off-site welding, no hot works |

| Limit required | $20 million | $5 to $10 million |

| Earthmoving | Operating earthmoving plant | No earthmoving |

| Revenue | Higher annual turnover | Lower annual turnover |

| Market access | Standard market only (declines) | Specialist agency via a broker |

The takeaway: a decline from the standard market doesn’t tell you what the cover should cost. In this case the spread between the cheapest and dearest terms was significant, and the difference came down to how the risk was presented and which markets were approached. If you also run plant on site, our guide to earthmoving and excavator insurance covers that side of the risk.

Frequently Asked Questions

Can a mine-site contractor get $20 million public liability insurance?

Yes. Even a sole trader working on mine sites can get $20 million public liability cover. It usually sits outside the standard market, though, so it has to be placed with a specialist liability underwriting agency, generally through a broker. Tank recently placed $20M cover for a WA mine-site subcontractor after much of the mainstream market declined.

Why do mining contractors get declined for public liability?

Mine-site work combines a high-risk environment, a high required limit (often $20 million), and frequently a sole-trader structure. That mix falls outside the appetite of most standard public liability insurers, so they decline rather than quote. The risk usually has to go to a specialist underwriting agency that assesses it by hand.

How much does $20M public liability cost for a mining subcontractor?

For a sole-trader mine-site subcontractor in 2026, comparable quotes ranged from around $3,200 to over $5,000 a year. We placed the cover at the bottom of that range, approximately $3,200, with a monthly option of around $260 a month. Your premium depends on your trade, revenue, mine types and machinery.

Do I need an active ABN to take out public liability insurance?

Often yes, at least to firm up a quote. Some insurers will give you indicative terms without one, but they usually make it a condition (a subjectivity) that you have a registered, active ABN, and they confirm that before they bind the final policy. You can check your status on ABN Lookup, and a cancelled ABN can be reactivated through the Australian Business Register (ABR).

Does public liability cover poly welding or HDPE poly pipe welding on mine sites?

It can, but the occupation has to be described accurately to the underwriter. Off-site poly-pipe welding with no workshop, no hot-works permits and no earthmoving is a different risk to fabrication or plant work. Getting that description right is often what makes the placement possible, and what keeps the premium sensible.

Getting the right cover for mine-site work

High-limit public liability for mining contractors is hard to place, but it’s far from impossible. A decline from the standard market usually means the risk needs a specialist underwriting agency and a broker who can access one, not that you’re uninsurable. Get the occupation described accurately, sort your ABN early, and leave time before your start date.

If you’ve been knocked back for $20 million public liability insurance, or you’ve been told you need a high limit for a mine engagement, that’s exactly the kind of hard-to-place risk we take on.

Need $20 million public liability for mine-site work? Tank Insurance specialises in hard-to-place liability risks. Talk to a Tank broker about mine-site public liability on 02 9000 1155 or [email protected] and we’ll work through your options.

This is general information only and does not take into account your objectives, financial situation, or needs. You should consider whether the information is appropriate for you and read the relevant Product Disclosure Statement (PDS) before making any decisions about insurance products.