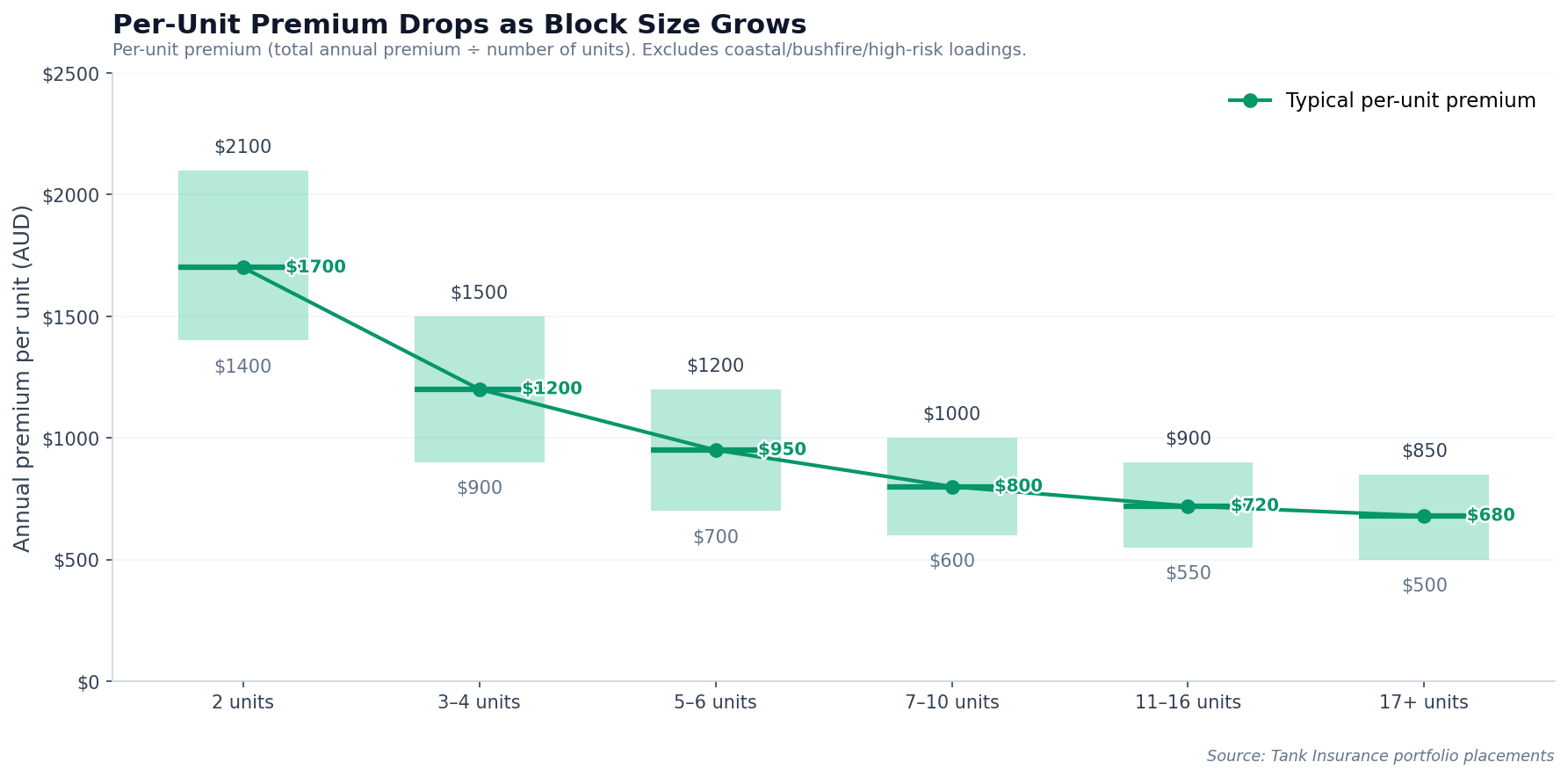

Block of units insurance isn't priced on a simple rate card. Premium depends on unit count, location, construction type, sum insured, claims history, and the mix of tenants in the building.

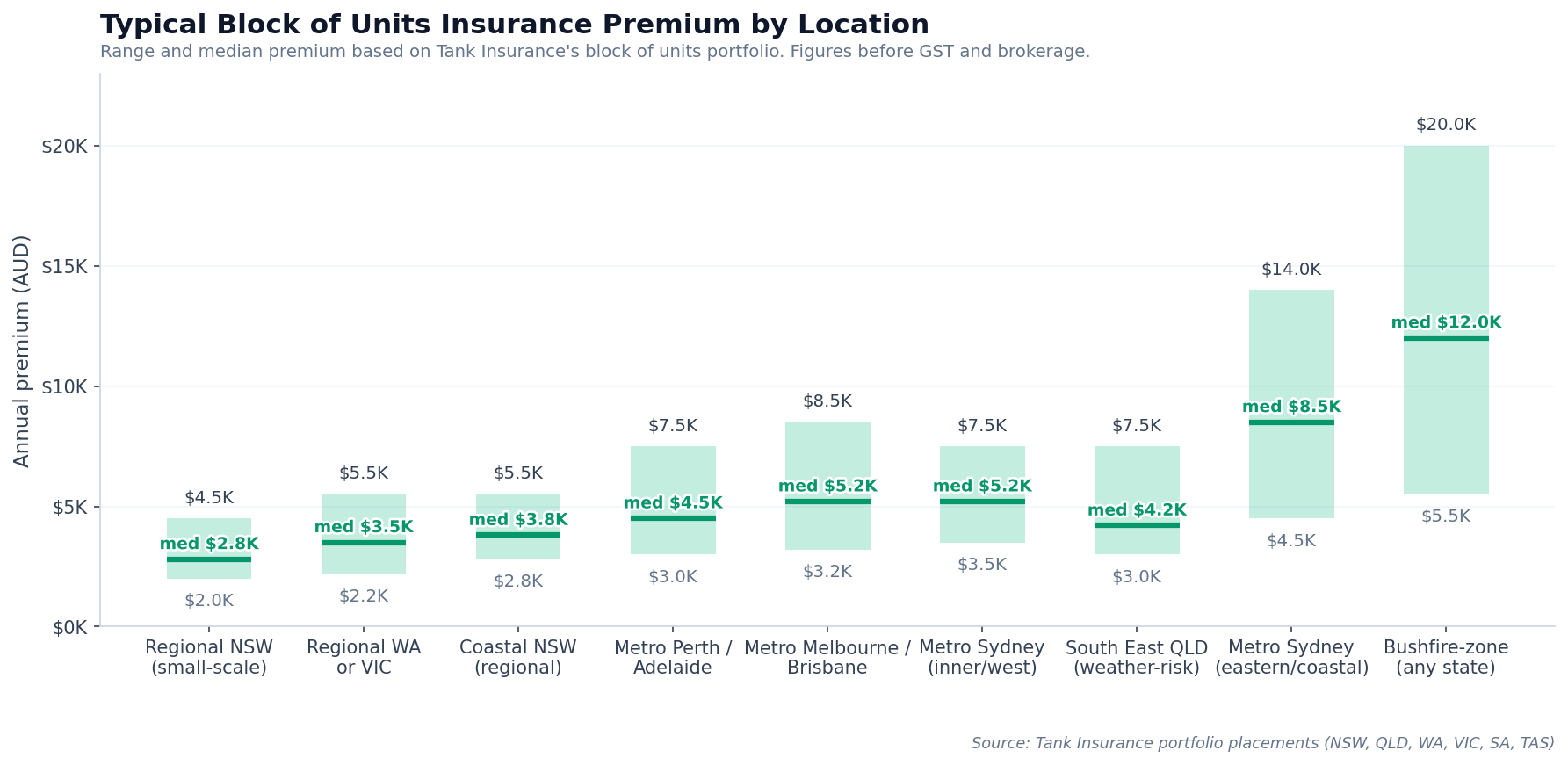

The ranges on this page come from Tank's actual placements across NSW, QLD, WA, VIC, SA and TAS. Every figure is drawn from real policies bound for real property owners - not insurer brochures or industry averages. Our portfolio average sits around $4,800 annually, with most placements landing between $2,000 and $10,000.

These figures are directional - drawn from Tank's block of units placements plus broker market experience, not strict per-deal statistics. Individual placements will sit above or below these ranges depending on the property's specific risk profile.

What you'll typically pay:

- Small regional blocks (2–4 units): roughly $2,000 to $4,500 a year

- Coastal regional blocks: roughly $2,800 to $5,500 a year

- Metro Sydney (inner/west): roughly $3,500 to $7,500 a year

- Metro Sydney (eastern/coastal): roughly $4,500 to $14,000 a year

- Metro Melbourne, Brisbane, Adelaide, Perth: roughly $3,000 to $8,500 a year

- Queensland coastal with cyclone + flood: roughly $3,000 to $7,500 a year

- WA / regional (non-coastal): roughly $2,200 to $5,500 a year

- Bushfire-zone or high-risk exposure (any state): $5,500 to $20,000+ a year

These are annual premium ranges - before GST and brokerage - for standard block of units cover including building, public liability and loss of rent. Higher-risk configurations (very large blocks, multiple prior claims, or overlapping flood/bushfire zones) can sit outside these ranges.