Contents

If you’re running a scaffolding business anywhere in Australia, you’ve likely noticed that insurance premiums can feel like a bit of a puzzle.

One quote might seem reasonable, while another feels like it’s blown the budget.

This is the case because they’re shaped by specific factors that reflect the unique risks and realities of your business.

Let’s have a look at the five key drivers of Scaffolding Insurance premiums and why they matter to you.

Key Takeaways:

- Scaffolding is a high-risk trade (falls from height account for 15% of worker fatalities), so premiums start higher than average

- Your annual turnover, number of employees, and whether your subbies have their own cover all directly affect what you pay

- A clean claims history is one of the strongest levers for keeping premiums down

- Bundling public liability with workers’ comp and ensuring subcontractors carry their own insurance can unlock savings

Why Scaffolding Insurance Costs More Than You Might Expect

Scaffolding isn’t your average trade. It involves working at heights, handling heavy equipment and navigating complex construction sites.

These realities make it a high-risk industry which directly impacts the cost of insurance.

Understanding what drives these costs can help you make smarter decisions when choosing cover and managing your business risks.

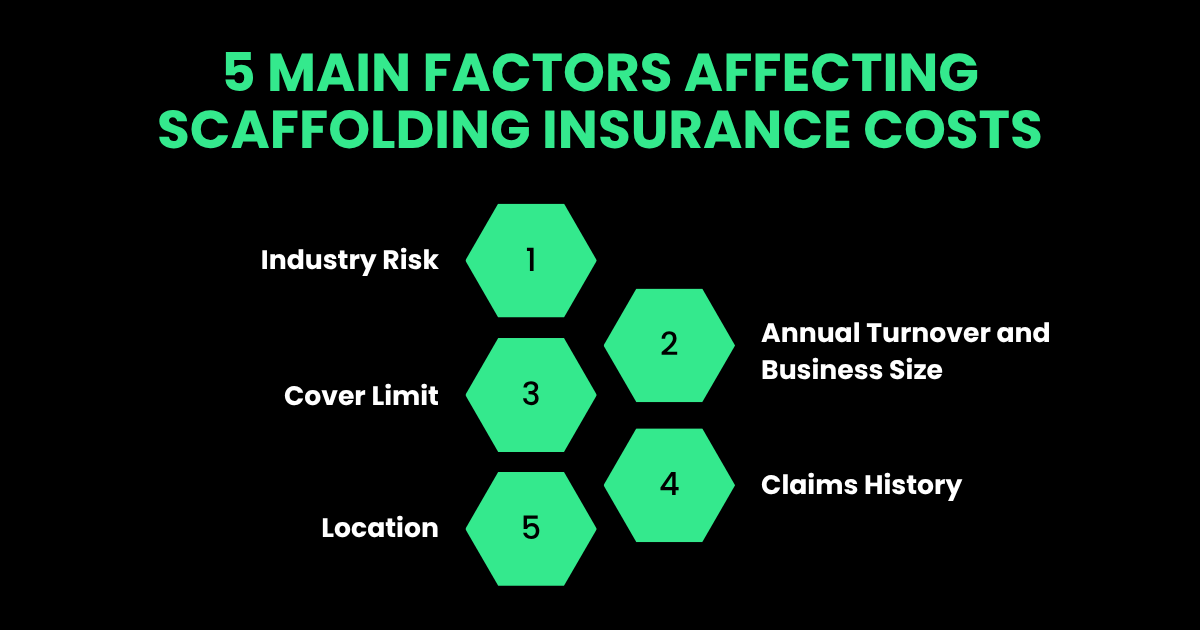

Here are the five main factors that shape your Scaffolding Insurance premiums:

- Industry Risk: Scaffolding work carries inherent risks, think working at heights, heavy machinery and exposure to busy construction sites.

These factors create a higher likelihood of accidents or injuries which insurers account for with a higher baseline premium.

For example, a report from Safe Work Australia noted that falls from height accounted for 15% of worker fatalities with scaffolding-related incidents being a significant contributor. This risk profile means scaffolding businesses often face higher premiums. - Annual Turnover and Business Size: The size of your business matters. Insurers look at your annual turnover and the number of employees or subcontractors you manage.

A larger turnover or workforce signals greater exposure to potential claims which pushes premiums up.

If you use subcontractors, their insurance coverage (or lack thereof) can also bump up your premium as insurers may see them as an added risk. - Cover Limit: The amount of cover you select directly affects your premium.

When you choose a higher coverage amount (e.g., higher liability limits or lower deductibles), the insurer may have to pay out more in the event of a claim. This increased potential payout raises their risk, leading to a higher premium to cover that exposure.

Choosing the right cover limit is about balancing compliance, client requirements and your budget. - Claims History: If your business has made claims in the past, insurers will take notice.

A history of frequent or costly claims, say for workplace injuries or property damage, can lead to premium increases.

Basically, a scaffolding company with a clean claims record might secure a more competitive rate while one with a recent claim could see their premium rise significantly.

Keeping a strong safety record and proactive risk management can help keep these costs in check. - Location: Your location plays a bigger role than you might think.

State-based taxes, like stamp duty, can add to your premium depending on where you are located.

Additionally, areas prone to natural disasters, such as cyclones or floods, can increase costs due to higher perceived risks. Urban areas, with higher population density and legal costs, also tend to have pricier premiums compared to rural regions.

How to Manage Your Scaffolding Insurance Costs

Understanding these factors is the first step to getting the right cover at a price that works for you.

Here are some practical tips to help keep your premiums manageable:

- Prioritise Safety: Invest in training and safety equipment to reduce the risk of claims. A strong safety record can lead to lower premiums over time.

- Shop Around: Insurance brokers, like us at Tank Insurance, can help you compare policies from multiple insurers to find you the best fit. Don’t settle for the first quote you get.

- Check Subcontractor Cover: Ensure your subcontractors have their own insurance to avoid premium hikes.

- Review Your Cover Limit: Work with a broker to choose a cover limit that meets your needs without overpaying for unnecessary protection.

- Bundle Policies: Combining Public Liability with other covers, like Workers’ Compensation, can sometimes unlock discounts.

Get the Right Cover Now

Scaffolding Insurance premiums are driven by the unique risks and realities of your business, from the high-risk nature of the work to your location and claims history.

By understanding these factors, you can make informed decisions and potentially save on costs.

If you’re ready to explore your options or just want to chat about what’s best for your business, reach out to us at [email protected] or call us at 02 9000 1155.

We’re here to help you find cover that fits your needs and budget!