Contents

A landlord came to Tank Insurance at renewal time. They’d been with a direct insurer for years, renewing automatically each year without much thought. The property was a small block of units in NSW - their main investment outside super.

When Brady on our team reviewed the policy, one number jumped out immediately. The sum insured - the maximum the insurer would pay to rebuild the property - hadn’t been updated in over six years. It was sitting at $600,000. The estimated replacement cost? Closer to $800,000.

That’s a $200,000 gap. And if something had happened - a fire, a major storm, a total loss event - the landlord would have been $200,000 short. The insurer only pays up to the sum insured.

Here’s what happened, how we fixed it, and why this matters for every landlord.

What was the problem?

The landlord had purchased the property years ago and set their sum insured based on the purchase price minus the land value. That’s a reasonable starting point - at the time.

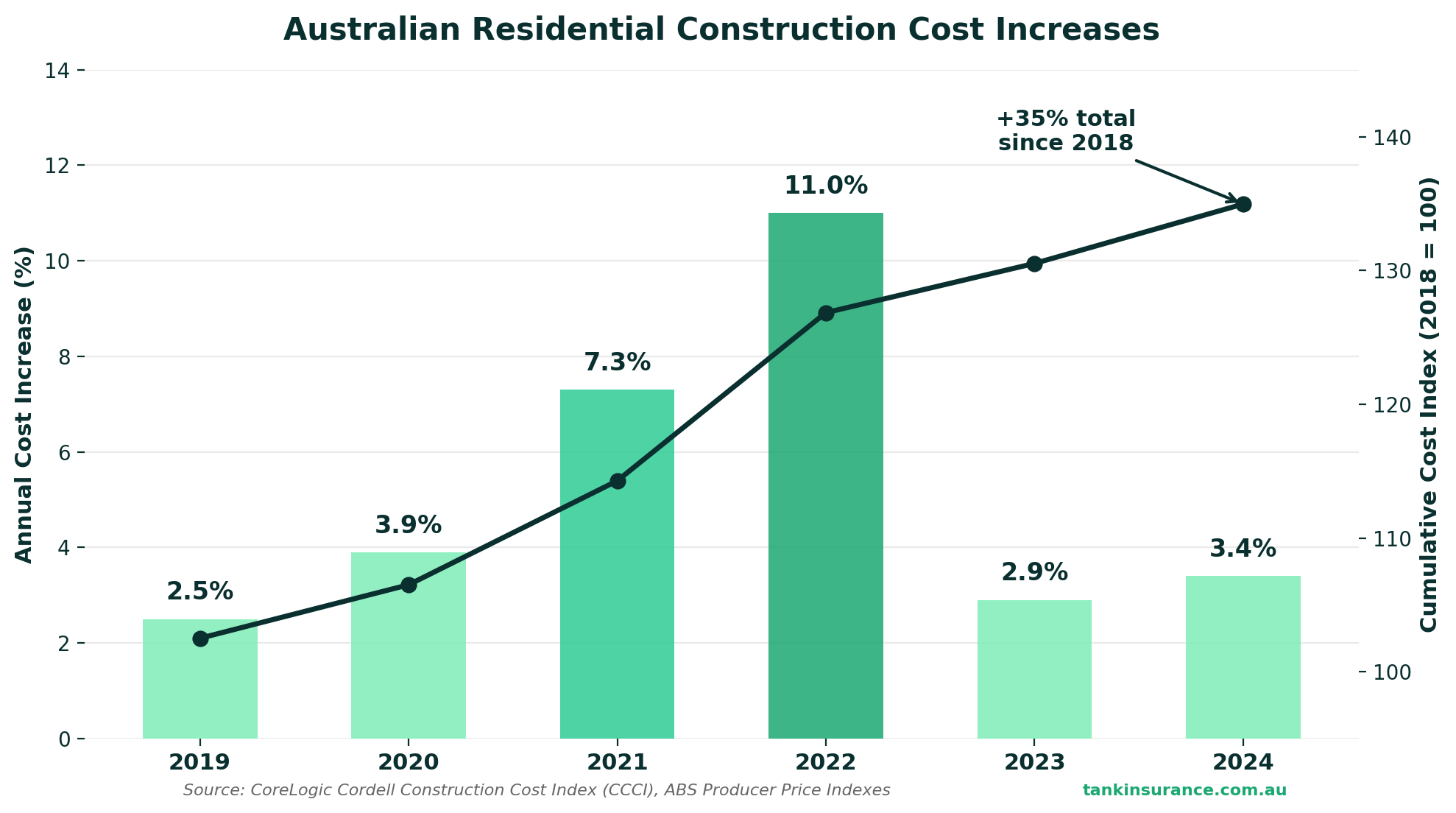

But construction costs don’t stand still. Between 2020 and 2025, residential construction costs in Australia increased by over 30%, with house construction prices rising as much as 40% in some areas. Materials, labour, and regulatory requirements all pushed rebuild costs higher.

The landlord’s sum insured had been indexed by the insurer’s automatic inflation adjustment each year - usually 3-5%. But that adjustment hadn’t kept pace with the actual increase in construction costs.

The result: a property that would cost approximately $800,000 to rebuild from scratch, insured for $600,000. That’s 75% of the replacement value.

Why does underinsurance matter?

Most people assume that if their property is insured for $600,000 and they have a total loss claim, the insurer rebuilds the property. But your insurer will only pay up to the sum insured. If the rebuild costs $800,000 and you’re insured for $600,000, you’re $200,000 out of pocket.

That’s the core risk with underinsurance for landlord insurance - your payout is capped at the sum insured. If that number hasn’t kept up with construction costs, you’re carrying the gap yourself.

It’s also worth knowing that some commercial property policies include an average clause (sometimes called a co-insurance clause) that reduces payouts proportionally on partial claims too. While this isn’t standard in most residential landlord policies, the principle is the same - if you’re underinsured, you’re exposed.

For this landlord, the sum insured was $200,000 short of the rebuild cost. In a total loss scenario, that’s $200,000 they’d need to find themselves.

We’ve covered the mechanics of underinsurance and the average clause in detail in our sum insured and underinsurance guide.

What did Tank do?

When Brady reviewed this at renewal, the fix was straightforward but the impact was significant.

Step 1: Flagged a potential gap

When Brady reviewed the policy, the sum insured looked low for the building type, size, and location. We flagged this with the landlord and recommended they get an independent replacement cost assessment - either through a quantity surveyor or by using industry rebuild cost calculators to estimate what it would actually cost to demolish and rebuild to current codes.

The landlord did their own checks and came back with a figure around $800,000 - including demolition, debris removal, professional fees, and compliance with current building codes. That confirmed the gap we’d suspected.

Step 2: Updated the sum insured

Based on the landlord’s updated replacement cost figure, we increased the sum insured from $600,000 to $800,000. This brought the property back to full replacement value.

Step 3: The cost difference

Here’s the part that surprises most landlords. Increasing the sum insured by $200,000 didn’t increase the premium by anywhere near as much as they expected.

The premium difference for the additional $200,000 in cover was modest - a few hundred dollars per year. Compare that to the $200,000 gap in a total loss scenario.

The landlord’s reaction was the same one we hear regularly: “Why didn’t anyone mention this before?”

With a direct insurer, there’s typically no one reviewing these things proactively at renewal. The policy auto-renews, the sum insured gets a small inflation adjustment, and the gap quietly grows wider each year.

How common is landlord underinsurance?

Very common. When we onboard new landlord clients at Tank, reviewing the sum insured is one of the first things we do. More often than not, the sum insured needs adjusting.

Common reasons landlord properties end up underinsured:

- Purchase price as sum insured - using the purchase price (minus land) as the sum insured, then never updating it

- Automatic inflation adjustments falling behind - insurer indexation of 3-5% per year hasn’t kept up with actual construction cost increases that significantly outpaced standard indexation, particularly between 2021 and 2023

- Renovations not reflected - a kitchen renovation, bathroom upgrade, or added granny flat that was never communicated to the insurer

- Building code changes - if the property was destroyed, it would need to be rebuilt to current building codes, which may be more expensive than when it was originally built

- Forgotten costs - demolition, debris removal, temporary fencing, council fees, architect and engineer fees, and compliance certificates all add to the rebuild cost and are often left out of the sum insured calculation

For properties that haven’t had a professional valuation in 5+ years, we regularly see gaps of 20-40% between the sum insured and the actual rebuild cost.

How to check if your property is underinsured

If you’re a landlord reading this and wondering whether your sum insured is right, here’s what to do:

1. Check your current sum insured

Look at your policy schedule or Certificate of Currency. The sum insured (sometimes called building sum insured) is the maximum the insurer will pay to rebuild.

2. Estimate the replacement cost

This is not the market value of the property. It’s not the purchase price. It’s the cost to demolish the existing building and rebuild from scratch to current building codes.

Include:

- Construction costs (per square metre for your building type and area)

- Demolition and debris removal

- Professional fees (architect, engineer, surveyor - typically 10-15% of build cost)

- Council fees and compliance costs

- Temporary fencing and site security

- Any improvements or renovations since the original build

3. Get a professional valuation

For the most accurate number, commission a replacement cost valuation from a qualified quantity surveyor. These typically cost $300-$600 and can save you tens or hundreds of thousands if you need to claim.

4. Talk to your broker

A broker reviews your sum insured at every renewal and flags anything that looks low. This is one of the basic but critical things a broker does that a direct insurer doesn’t.

What about blocks of units and multi-property portfolios?

For landlords with multiple properties or blocks of units, underinsurance risk multiplies. Each property needs its own accurate sum insured, and the costs of getting it wrong scale with the portfolio.

Brady on our team manages multi-property landlord portfolios and reviews every sum insured at renewal. For blocks of units specifically, the sum insured needs to cover the entire building - not just one unit. This includes common areas, shared infrastructure (plumbing, electrical, roofing), and any outbuildings.

Frequently Asked Questions

What is underinsurance for landlords?

Underinsurance means your sum insured is less than the actual rebuild cost. If you’re underinsured and make a total loss claim, the insurer only pays up to the sum insured - you cover the gap yourself.

How does the average clause work in insurance?

The average clause (or co-insurance clause) is mainly found in commercial property policies. It reduces your claim payout proportionally based on how underinsured you are. While it’s not standard in most residential landlord policies, the core risk is the same - if your sum insured is less than the rebuild cost, you’re carrying the difference yourself.

How often should landlords review their sum insured?

At every annual renewal at a minimum. Get a professional replacement cost valuation every 3-5 years, or sooner if there’s been significant construction cost inflation, major renovations, or building code changes.

Is market value the same as replacement value for insurance?

No. Market value includes land (which doesn’t need rebuilding). Replacement value is the cost to demolish and rebuild the structure to current codes, including demolition, debris removal, professional fees, and compliance costs.

Worried about your sum insured?

If you’re a landlord and you’re not sure whether your sum insured is accurate, let’s check. It takes five minutes at renewal and could save you hundreds of thousands in a claim.

Tank Insurance is an Australian broker specialising in landlord insurance. We review every policy at renewal - including the sum insured - because getting this number right is one of the most important things we do.

Call us on 02 9000 1155 or email [email protected].

This is general information only and does not take into account your objectives, financial situation, or needs. You should consider whether the information is appropriate for you and read the relevant Product Disclosure Statement (PDS) before making any decisions about insurance products.