Contents

You give advice for a living. You also visit client sites, meet people face-to-face, and work in spaces where someone could trip over your laptop bag. So which insurance covers what?

This is the question we hear more than almost any other at Tank Insurance. And it’s a good one - because professional indemnity insurance and public liability insurance cover completely different risks, and mixing them up can leave you seriously exposed.

Here’s the short version: PI covers your brain. PL covers your body (and everyone else’s). But the full picture matters, so let’s break it down.

Key Takeaways:

- Professional indemnity (PI) covers claims arising from your advice, designs, or professional services

- Public liability (PL) covers injury to people or damage to their property

- Many businesses need both - but the mix depends on what you do

- Getting the wrong one (or the wrong limit) is one of the most common mistakes we see

What is professional indemnity insurance?

Professional indemnity insurance is a policy that protects you when a client claims your advice, service, or professional work caused them a financial loss.

Think of it as cover for the “thinking” side of your business. If you design something, recommend something, consult on something, or sign off on something - and it goes wrong - PI is what responds.

It typically covers:

- Legal defence costs - even if the claim has no merit

- Compensation payouts - if you’re found liable

- Breach of professional duty - errors, omissions, negligence

- Intellectual property disputes - in some policies

- Document loss or damage - for certain professions

PI is what many engineers carry when they sign off on structural calculations. It’s what IT consultants carry when they recommend a system that crashes. And it’s what accountants carry when a tax return has an error.

Over the last 12 months alone, we’ve placed PI cover for businesses across dozens of industries - from engineers and architects to management consultants and IT firms. The pattern we see? What we’re commonly hearing is questions around the two and how they differ.

Jack O’Hagan, one of our senior insurance brokers says, “The common thread is that if your work involves giving advice or delivering a professional service, PI is usually on the table. And in 2026, we’re seeing more contracts requiring it than ever.”

What is public liability insurance?

Public liability insurance covers claims when someone who isn’t your employee gets injured, or their property gets damaged, because of your business activities.

This is the “physical” side of things. A client visits your office and slips on a wet floor. You’re working on a job site and a tool falls onto someone’s car. A customer has an allergic reaction to a product you sold.

PL typically covers:

- Third-party bodily injury - medical costs, rehabilitation, compensation

- Third-party property damage - repair or replacement costs

- Legal defence costs - solicitors, barristers, court fees

- Products liability - in many policies, claims arising from products you’ve sold or supplied

What’s the actual difference between PI and PL?

The core difference is the type of harm your business causes.

Professional indemnity responds when your advice or professional work causes a financial loss. Public liability responds when your business causes physical injury or property damage.

Here’s a side-by-side comparison:

| Professional Indemnity (PI) | Public Liability (PL) | |

|---|---|---|

| What it covers | Financial loss from your advice or services | Physical injury or property damage to third parties |

| Type of harm | Economic/financial | Physical/bodily |

| Trigger | Client claims your work was negligent or incorrect | Someone is injured or their property is damaged |

| Policy type | Claims-made (when the claim is made matters) | Occurrence-based (when the incident happened matters) |

| Who typically needs it | Consultants, engineers, accountants, architects, IT professionals | Tradies, retailers, hospitality, any business with public interaction |

| Common limits | $1M, $2M, $5M, $10M, $20M | $5M, $10M, $20M |

| Legal defence | Yes - included | Yes - included |

One important distinction: PI policies are claims-made, meaning the policy that responds is the one in force when the claim is lodged - not when the work was done. PL policies are typically occurrence-based, meaning the policy in force when the incident happened is the one that responds.

This is why run-off cover matters if you ever stop trading or retire with PI in place.

Can you give me a real-world example?

Sure. Here’s how the same scenario plays out differently depending on the type of claim.

Scenario: An engineer visits a client’s warehouse

- The engineer inspects the building and provides a structural assessment report saying the mezzanine floor is safe for heavy storage.

- Three months later, the mezzanine floor develops cracking. The client has to close the warehouse for repairs and loses $150,000 in revenue.

PI claim: The client sues the engineer, alleging the structural assessment was negligent. The engineer’s professional indemnity policy responds - covering the legal defence and any settlement or award.

Now imagine a different outcome from the same visit:

- While inspecting the warehouse, the engineer accidentally knocks a fire extinguisher off the wall. It hits the client’s forklift, cracking the windscreen and denting the bonnet.

PL claim: The client sends a bill for $4,800 in forklift repairs. The engineer’s public liability policy responds.

Same engineer, same client, same visit. But completely different policies responding to completely different risks.

This kind of dual-risk situation isn’t unusual. A consulting firm with only PI in place, not realising that the site visits they do every week create a separate liability exposure.

Do I need both PI and PL?

Many businesses need both. But not all.

Here’s a general guide based on what your business does:

PI is typically relevant if you:

- Give advice, recommendations, or professional opinions

- Design, specify, or certify anything

- Provide consulting or professional services

- Handle client data or documents

- Are required to hold it by law, regulation, or contract

PL is typically relevant if you:

- Have clients or the public visiting your premises

- Work on other people’s property

- Sell or supply physical products

- Run events or activities

- Operate in any physical environment where injury could occur

Both are often needed if you:

- Provide professional services AND visit client sites (engineers, architects, surveyors)

- Run a business with customer-facing operations AND provide advice (financial planners with office foot traffic)

- Are a builder or design-and-construct contractor who both designs and physically builds

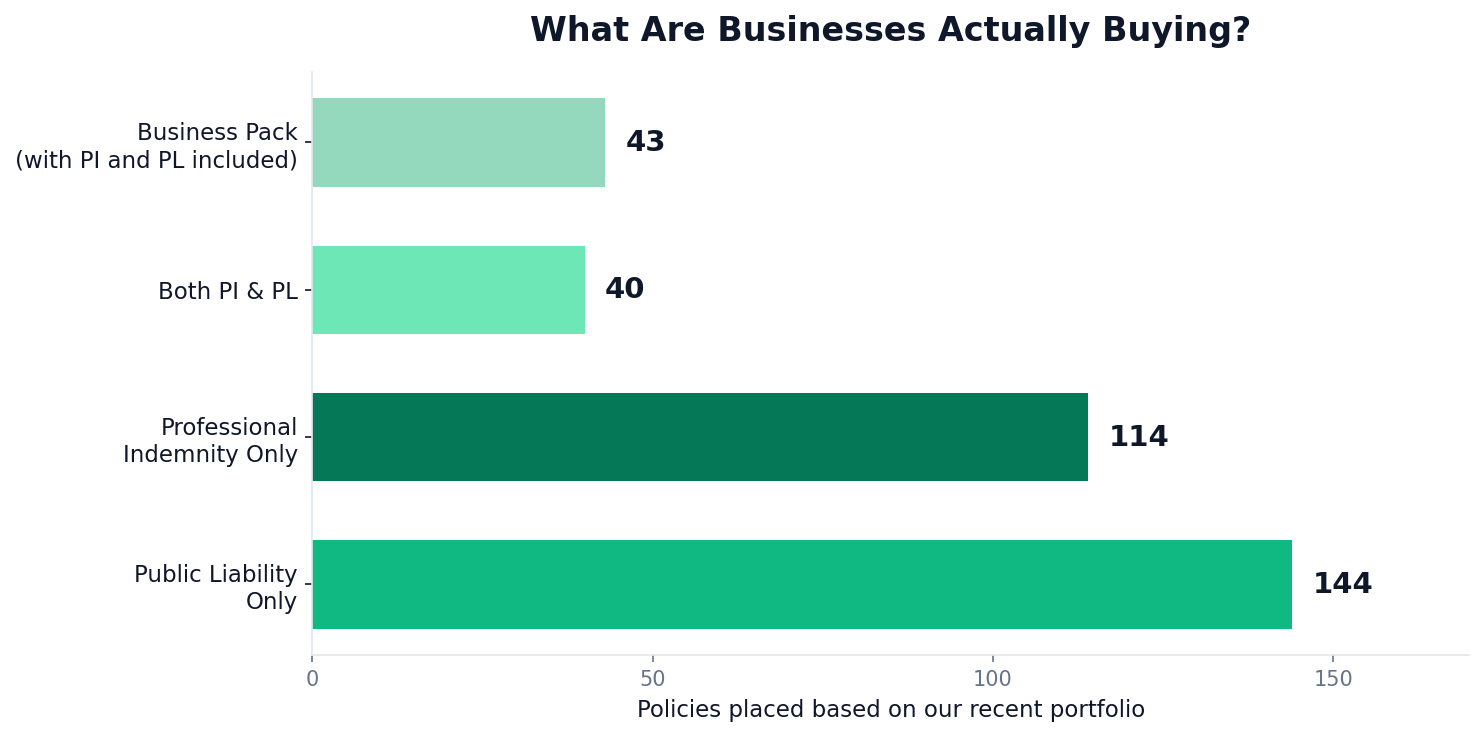

Based on our recent portfolio, here’s what businesses are actually taking up:

Some industries are required by legislation to hold PI. For example, registered design practitioners - including engineers providing regulated designs for Class 2 buildings (apartments) in NSW - must hold PI under the Design and Building Practitioners Act 2020. Financial services licensees may also need PI as part of ASIC’s compensation arrangement requirements. And most commercial leases and contracts will require PL as a minimum.

How much does each type of cover cost?

Premiums vary significantly depending on your industry, revenue, claims history, and the limits you need. There’s no single answer - but here are the factors that drive cost for each.

What affects PI premiums:

- Your profession and the type of advice you give

- Annual revenue or fee income

- Claims history (this is a big one)

- The retroactive date on your policy

- Limit of indemnity and excess

What affects PL premiums:

- Your industry and what you physically do

- Annual turnover

- Number of employees

- Whether you work on other people’s property

- Claims history

For business insurance in general, the best way to understand what you’ll pay is to talk to a broker who can assess your specific situation. Premiums for PI and PL can range from a few hundred dollars for low-risk sole traders to tens of thousands for larger firms in high-risk industries.

What happens if I have the wrong cover?

This is where it gets painful.

If someone sues you for negligent advice and you only have PL - your insurer would likely decline the claim. PL doesn’t respond to professional negligence. You’d be defending yourself out of pocket.

The reverse is also true. If a visitor slips in your office and you only have PI - same problem. PI doesn’t cover bodily injury to third parties.

It’s not uncommon for businesses to discover this kind of gap the hard way. A management consultant with PL only who faces a negligence claim. A trades business with PI only who then has a public injury incident on a job site.

The fix is straightforward - but it’s much cheaper to sort out before a claim than after one.

Frequently Asked Questions

Is professional indemnity the same as public liability?

No. Professional indemnity covers financial losses caused by your professional advice or services. Public liability covers physical injury or property damage to third parties. They protect against different types of risk and most businesses that need one should consider whether they also need the other.

Do sole traders need professional indemnity insurance?

It depends on what you do. If you provide advice, consulting, design work, or any professional service - yes, PI is typically important regardless of your business structure. Being a sole trader doesn’t reduce your exposure to a negligence claim.

Can I get PI and PL in one policy?

Sometimes. Some insurers offer combined policies or business packs that bundle PI and PL together. Whether this makes sense depends on your industry and the limits you need. A broker can help you work out whether bundling or separate policies gives you better cover and value.

What PI and PL limits do I need?

There’s no one-size-fits-all answer. Common PI limits range from $1 million to $20 million depending on your profession, project sizes, and contractual requirements. PL limits of $10 million or $20 million are standard for most businesses. Your contracts, industry regulations, and risk profile should guide the decision.

Does public liability cover my employees?

No. PL covers injury to third parties - ie, people who aren’t your employees. If an employee is injured at work, that’s covered by workers compensation insurance, which is a separate (and compulsory) requirement in every Australian state and territory. You can find more on workers compensation obligations at Safe Work Australia.

Getting the Right Cover

The difference between professional indemnity and public liability comes down to what your business does and what could go wrong. PI covers the advice. PL covers the physical.

Most businesses we work with need at least one. Many need both. And the ones that get caught out are usually the ones who assumed one policy covered everything.

If you’re not sure which cover fits your situation, it’s worth having a quick conversation with a broker who understands your industry.

Need help working out the right mix of PI and PL for your business? Tank Insurance specialises in both. Reach out to our team at 02 9000 1155 or [email protected] to chat through your options.

This is general information only. It doesn’t take your specific situation into account. Always read your Product Disclosure Statement and policy wording, and get advice for your circumstances.